Inflation Reaches 40-Year High

On June 10, 2022, the Bureau of Labor and Statistics released the May Consumer Price Index report. The report shows inflation has increased by 8.6% since May 2021. The report does not include food, energy, or housing to determine the inflation rate. Essentially, the number says that a product that cost $100 in May 2021 would now cost $108.60.

According to Mark Zandi, chief economist at Moody’s Analytics, the average U.S. household spent $460 more per month to purchase the same items. If inflation does not rise higher, this trend will equate to $5,520 less to save or invest per year than in 2021. Wages will not keep up with inflation in 2022. Employers have only budgeted 3.4% for cost-of-living increases. This means that most Americans have at least 5.2% less purchasing power than one year ago (8.6% inflation rate – 3.4% Cost of living increase=5.2% decrease in purchasing power).

Inflation steals everyone’s purchasing power, but inflation hurts lower-income households the most. Higher prices represent a higher percentage of net income and available cash for lower-income households. The U.S. household median income is $61,937. $460 equates to 7.43% of the median income. and 20.8% of the monthly income of a family of 4 at the poverty line ($26,500). Approximately 54% of American households earn less than $75,000 per year.

When Americans lose purchasing power, several economic dominoes get knocked over. Money becomes a significant stress point for most Americans. People tend to focus on their most immediate needs as purchasing power decreases. Less money is available for investment and savings, which will create costly future problems. The more immediate effect of less disposable income is many people will cut out non-essential items and services like streaming services, gym memberships, and travel.

As people buy fewer goods and services, businesses must lower prices to bring consumers back into the market. Lower prices mean lower profits. Lower profits mean businesses need to cut costs or go out of business. The most expensive cost for most employers is wages and benefits.

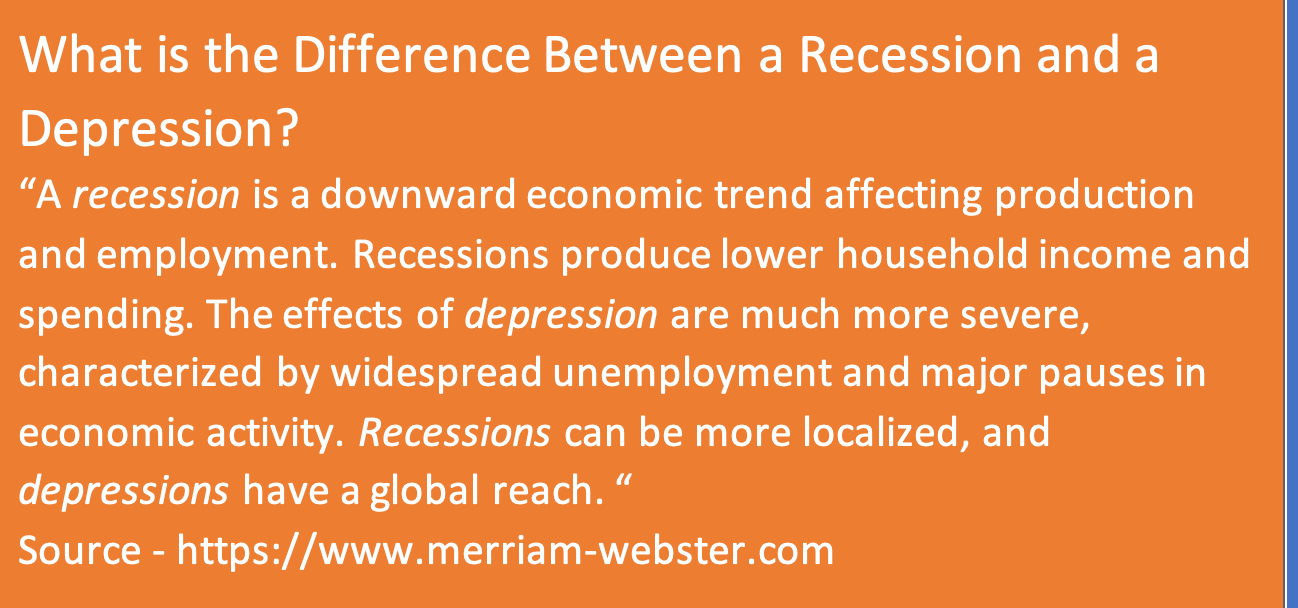

Businesses will look for the fastest ways to salvage profits if the worst happens too quickly. The most common business strategy is a massive layoff or a 'strategic restructure,' as they call them now. Coinbase, the largest cryptocurrency platform, lost $34 billion over the weekend and just laid off 18% of its full-time staff. Redfin, the real estate giant, also laid off 8% of their workforce. Unemployment will cause many people to lose even more purchasing power and be a catalyst for the cycle to repeat at a faster rate. It can quickly accelerate and become a death spiral to the bottom. In other words, high inflation often leads to a full-blown recession or depression.

There is a clear and present economic danger when Americans need to tighten their financial belts. People become more likely to default on debt obligations. The stock market crashed in March 2020. The following months saw a significant increase in people not paying their mortgage. The numbers were comparable to 2009, leading to a moratorium on evictions and foreclosures during the covid pandemic. Inflation in 2020 was only 1.4%, but it is 8.6% now.. Housing prices had increased by 6.14% in 2020. Housing has increased by 17.52% in 2022.

Most taxing authorities have reassessed property values to reflect the housing price increases. Higher taxes have increased most monthly mortgage payments (the escrow portion of the payment). A higher tax assessment caused the author’s monthly payment to increase by more than $250 on the property purchased one year ago.

Since 56% of Americans could not pay for a $1,000 emergency, this could quickly become a disaster.

Inflation has interest rates rising quickly. The current rate for a 30-year mortgage is 6.505% (6/13/22), and the Federal Reserve committed to raising rates at least 50 basis points (0.5%) on June 15, 2022. Some analysts are saying 75 basis points is a strong possibility. For example, a 75-basis point interest rate hike would equate to an additional $310 mortgage payment per month for every $100,000 borrowed. Eventually, housing prices will probably have to decrease so buyers can afford the monthly payment. The price correction could be mild or cataclysmic. Since the Dallas Federal Reserve released a recent paper saying housing shows signs of a bubble, most analysts think it could be severe.

Most people do not appreciate how severe the danger is. Sadly, most people are wildly unprepared for the predictable chain of events high inflation brings. People are losing purchasing power faster than they realize. Inflation has become "what is," but most people do not want to ask themselves the hard "what ifs ."What if history repeats itself? What if inflation eats away all my savings? What if people cannot pay their mortgages and the global economy collapses? What if the recovery takes a decade or more?

There are completely different ‘what ifs’ that can be asked. What if I had a plan and could do something today to protect my family? What if a single phone call could offer a time-tested solution?

Gold and other precious metals tend to be one of the best safe havens during high inflation and market crashes. Inflation is the primary danger to your wealth and purchasing power and stresses every area of the global economy. For some people, the recent inflation numbers are unfathomable. However, most people reading this article were alive during the inflation of the late 70s. Did you know gold went from $110 in 1976 to $850 in 1980 and from around $740 in 2008 to around 1900 in 2011? Physical precious metals are tangible assets with intrinsic value, essentially the opposite of paper assets. Precious metals have protected purchasing power for thousands of years.

Successful investors diversify their portfolios and put a percentage of their portfolios into precious metals. Some metals are better for short-term liquidity, and others are better for long-term growth. Usually, the best strategy is to have healthy amounts of both short and long-term metals in a portfolio. The experts at the U.S. Gold Bureau will educate you and help you choose the best metals for your situation. Act before inflation gets worse.

Will You Do What is Necessary to Protect Your Family?

Get Our Free

Gold & Silver

Investor's

Guide